Life Insurance & Estate Planning

Right after you pass away, your family has an immediate need for money. Life insurance pays your beneficiaries directly, quickly, and most of the time, income tax free. While many clients come to us thinking they no longer need life insurance in retirement, they are ignoring their surviving spouse (if married), funeral costs, and estate settlement costs.

Estate planning, especially estate planning documents, such as Wills and Power of Attorneys, are regarded as something only needed when you are younger and working, with children and a mortgage.

The ultimate goal of both life insurance and estate planning is to make sure your family and loved ones are taken care of, at least financially, after you pass. They are just as important in retirement as they are during your working years.

Questions we can answer

- How much life insurance should I have?

- Do I still need life insurance in retirement?

- Can I get life insurance with my pre-existing conditions?

- What does estate planning entail in retirement?

- Does my Will need to be updated or re-done entirely?

Life Insurance Quote

Cardinal Lessons on Life Insurance & Estate Planning

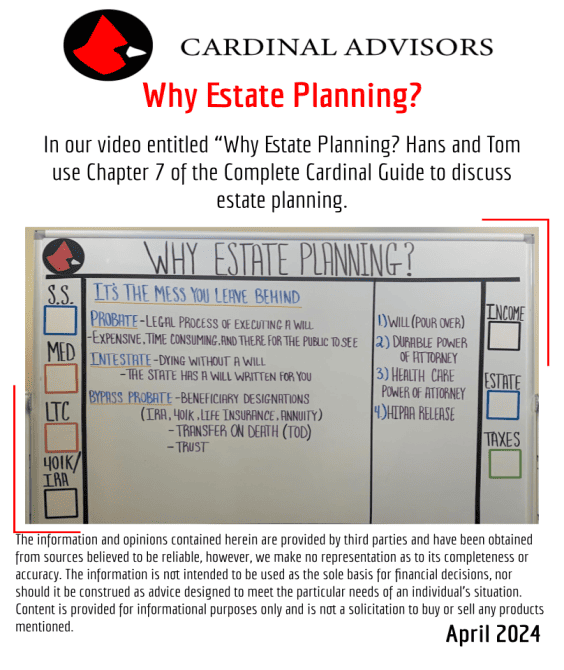

Why Estate Planning?

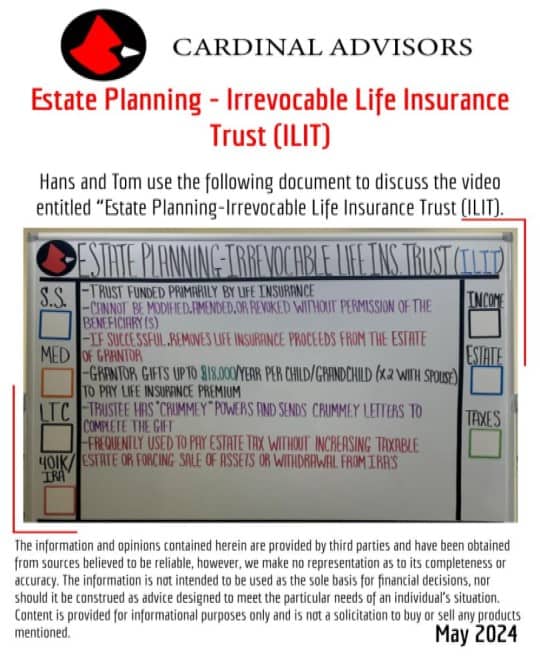

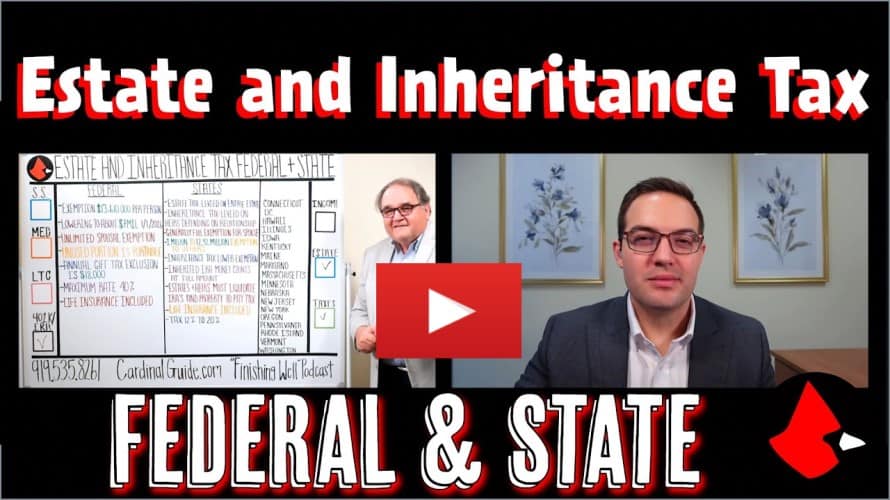

Estate and Inheritance Tax Federal & State

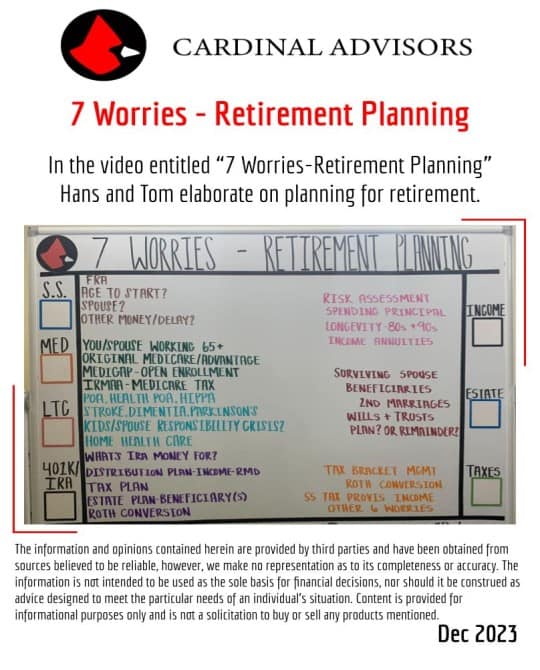

7 Worries – Retirement Planning

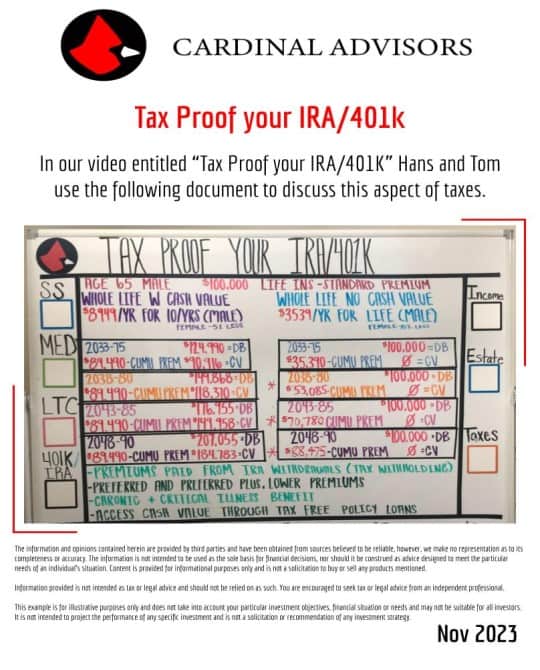

Tax Proof Your IRA/401k

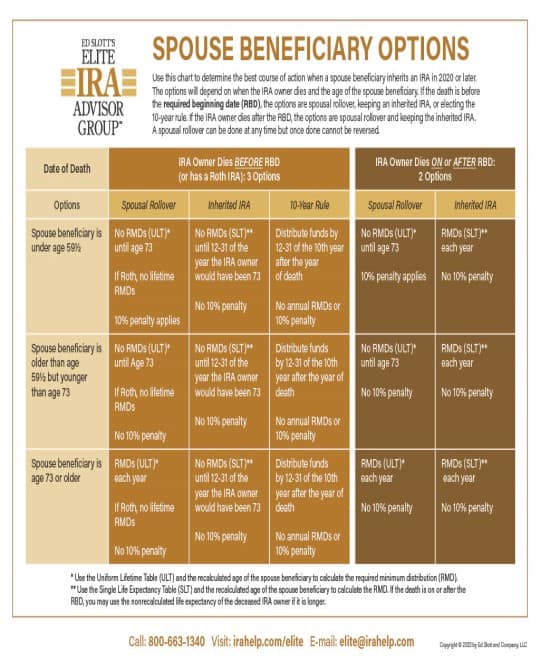

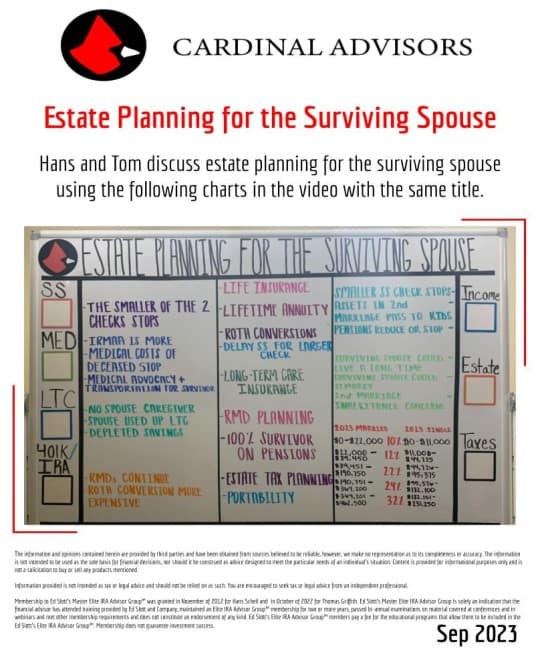

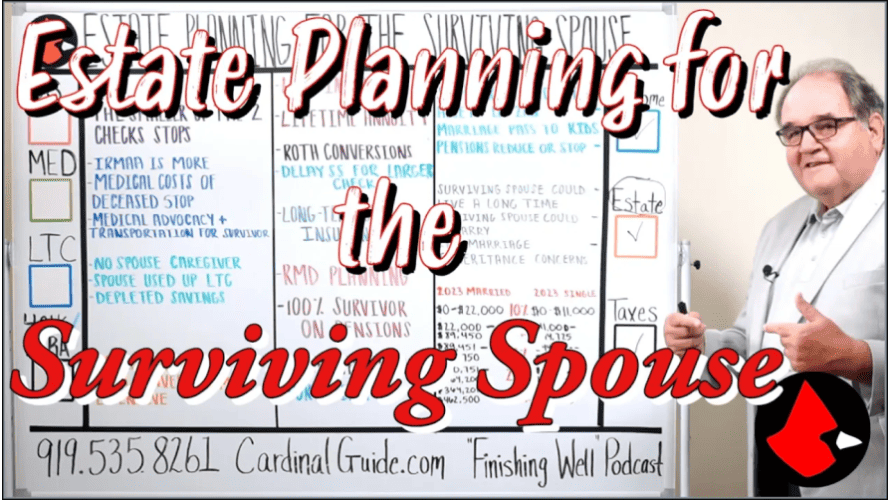

Estate Planning for the Surviving Spouse

Retirees Running Out of Money Late in Life

Special Needs Trust (SNT) Person With Disability (PWD)

IRA/401k=Lousy Estate Planning Strategy

Who Is Your Designated Beneficiary?

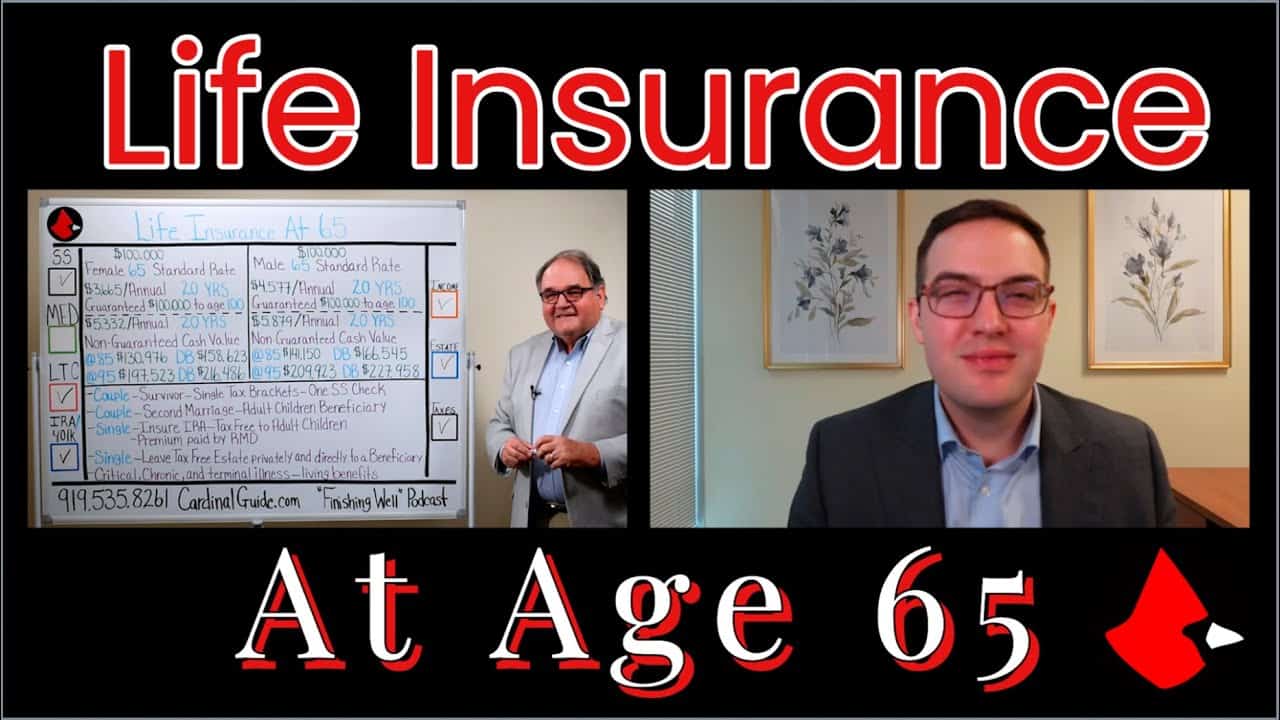

Life Insurance At Age 65

Seven Worries in Retirement Explained

Estate Planning

The Cardinal Guide To: Life Insurance & Estate Planning

Listen to learn:

There are different types of life insurance policies for retired people. Some have ongoing premiums while others can be paid all at once with a lump sum. There are even policies that allow you to use some of the life insurance benefit early if you need long term care.

Most people in retirement should have at least $25,000 of life insurance. Life insurance money is paid out swiftly to your beneficiaries. Payouts from your estate can take months or years. A small amount of life insurance allows them to quickly pay immediate expenses without having to go through the probate court.

Updating your life insurance beneficiary designations regularly is important. A designated beneficiary trumps your Will with benefits going straight to the named beneficiary.

Married couples who leave the entirety of their estate to each other need to consider who the ultimate beneficiaries are after the second spouse dies, especially if they are in a second marriages and have stepchildren. We have many clients who purchase separate life insurance policies naming specific children and stepchildren as beneficiaries.

When the first spouse passes, the smaller Social Security check stops. Life insurance is used to replace the lost income for the surviving spouse.

You need at least four legal documents prepared by an attorney knowledgeable about elder law: (1) a will, (2) a health-care power of attorney, (3) a financial power of attorney, and (4) a HIPAA release. These documents will instruct the court how your family is cared for after you pass, as well as give your family legal authority to care for you, in the way you want, while you are living.

Federal estate taxes likely do not apply unless your estate is worth more than $11.7 million ($22.4 million for couples) in 2021. The step up in basis for capital assets at death in calculating capital gains taxes for heirs is the more relevant issue for middle-class taxpayers.

Get In Touch

Contact us today with any questions, concerns, or just to stay connected.